Revenue-based funding lets businesses access capital by pledging a percentage of future revenue rather than giving up equity or putting up collateral. Payments flex with your actual sales—higher when business is strong, lower during slower months.

This guide covers how revenue-based funding works, who it's best suited for, and the tradeoffs you'll want to weigh before pursuing it.

Revenue-based funding is a type of financing where investors provide capital in exchange for a percentage of a company's ongoing gross revenues. Unlike traditional loans with fixed monthly payments, repayments rise and fall based on how much revenue your business actually generates. This makes it particularly well-suited for subscription-based businesses or e-commerce companies with predictable cash flow.

The arrangement continues until you've repaid a predetermined cap—typically 1.1x to 1.5x the original funding amount. So if you receive $500,000 with a 1.3x cap, you'll repay $650,000 total, regardless of how long it takes.

What sets revenue-based funding apart from other financing options is that founders keep full ownership of their company. There's no equity stake given up, no board seats surrendered, and no dilution of your ownership percentage. Here's what defines this model:

The mechanics are straightforward once you understand the core components. Let's walk through how a typical arrangement unfolds.

A funding provider advances you a lump sum based on your monthly recurring revenue or gross revenue. The amount you qualify for typically ranges from one to six months of your average monthly revenue, though this varies by provider and your business profile.

The repayment cap represents the total amount you'll pay back—your original funding plus a fee. This cap is fixed at the outset, so you know exactly what you owe from day one.

Each month, a fixed percentage of your revenue—typically 1-10%—is automatically collected. During a strong month, you pay more and accelerate your payoff. During a slower month, your payment decreases, giving your cash flow room to breathe.

Once you've paid back the full cap amount, the funding relationship ends. There's no ongoing obligation, no lingering interest accrual, and no balloon payment waiting at the end.

For the right business, revenue-based funding offers advantages that traditional financing can't match.

You maintain complete ownership of your company. For founders who've worked hard to build something valuable, this means not giving away a piece of the upside when your business eventually exits or scales significantly.

This is where revenue-based funding truly shines. If your revenue dips during a slow season or unexpected downturn, your payments automatically decrease. You're not stuck making a fixed payment that strains your cash flow when you can least afford it.

While bank loans can take weeks or months to close, many revenue-based funding providers make decisions within days. The underwriting process relies heavily on your revenue data, which can be verified quickly through integrations with your accounting software or payment processors.

Traditional bank loans often require personal guarantees or asset collateral. Revenue-based funding typically doesn't—your future revenue serves as the basis for the arrangement, keeping your personal assets separate from your business financing.

Revenue-based funding is designed for companies investing in growth initiatives like marketing spend, inventory purchases, or hiring. It's capital meant to generate returns, not fund long-term infrastructure projects.

No financing option is perfect for every situation. Understanding the limitations helps you make an informed decision.

Because you're paying back a multiple of what you borrowed, the effective cost often exceeds what you'd pay on a traditional bank loan. A 1.3x cap on a 12-month repayment translates to a significantly higher annualized rate than most term loans.

Revenue-based funding providers evaluate your ability to repay based on existing revenue patterns. If you're pre-revenue or have inconsistent sales, you likely won't qualify. This isn't startup funding—it's growth capital for businesses with traction.

Since your funding amount ties directly to your current revenue, you might not access as much capital as you'd get through equity financing or a large credit facility. For major expansion plans, revenue-based funding might only cover part of what you're looking for.

Many providers collect daily or weekly rather than monthly. While this smooths out cash flow in some ways, it also requires consistent revenue and careful cash management to avoid shortfalls.

Revenue-based funding works exceptionally well for certain business models while being a poor fit for others.

Predictable monthly recurring revenue makes repayment modeling straightforward for both you and the provider. The subscription model's inherent predictability is exactly what revenue-based funding is designed around.

Steady transaction volume provides the reliable revenue stream that supports percentage-based repayment. Seasonal businesses can still qualify, though providers will factor in revenue fluctuations.

Higher gross margins mean you can absorb the percentage-based repayment without squeezing your operating budget. A business running on thin margins might find the revenue share too constraining.

If maintaining ownership is a priority—whether for personal reasons or because you believe your equity will be worth significantly more later—revenue-based funding lets you access growth capital without giving up a stake.

Before applying, it helps to understand what providers typically look for during underwriting.

Most providers set a floor for monthly revenue, though the specific amount varies widely. Higher revenue generally means access to larger funding amounts and potentially better terms.

Providers want to see operating history to assess your revenue stability and trajectory. A longer track record with consistent growth strengthens your application.

You'll provide access to financial records, bank statements, or accounting software. Providers that use independently verified data can often move faster and offer more competitive terms because they have higher confidence in the numbers.

Funding amounts typically range from one to six months of your monthly revenue, though some providers go higher for established businesses with strong metrics. The specific amount depends on your revenue consistency, business model, and the provider's risk assessment.

Stronger documentation and verified data can improve your funding terms. When providers can independently confirm your revenue figures, they're often willing to offer larger amounts or lower repayment caps.

The application process is generally faster than traditional lending, but preparation still matters.

Gather your revenue documentation, bank statements, and accounting records before you start. Platforms that provide independently verified data can streamline this process significantly.

Complete the provider's application with your business information and revenue details. Many providers offer online applications that take 15-30 minutes.

Review repayment caps, revenue share percentages, and terms across multiple providers. The lowest cap isn't always the best deal—consider the revenue share percentage and how it affects your monthly cash flow.

Once you agree to terms, funds typically arrive within days. Some providers can fund within 24-48 hours of approval.

If revenue-based funding doesn't fit your situation, several other financing options might work better.

Modern platforms have transformed how revenue-based funding transactions happen. Real-time data integration and automated reporting allow providers to verify revenue, monitor performance, and manage risk far more efficiently than manual processes ever could.

For originators and investors in the revenue-based funding space, technology solutions that provide independently verified data and real-time monitoring support faster, more transparent funding decisions. Platforms like Cascade Debt enable this kind of infrastructure, helping both sides of the transaction operate with greater confidence and efficiency.

Revenue-based funding offers flexible, non-dilutive capital for businesses with proven revenue streams. The key is honestly assessing whether your revenue history and business model align with what providers look for.

If you're an originator or investor looking to streamline revenue-based funding operations with verified data and real-time analytics, Get Started with Cascade Debt.

Your payments decrease proportionally since they're tied to a percentage of revenue. This built-in flexibility protects businesses during slower periods—you won't face a fixed payment you can't afford when revenue is down.

Revenue-based funding is structured as debt because it requires repayment. However, it doesn't involve giving up ownership like equity financing, which is why it's often called "non-dilutive" capital.

Generally, no. Revenue-based funding requires demonstrated revenue history for underwriting. Pre-revenue startups typically explore other options like equity financing, grants, or convertible notes.

Providers typically require access to bank statements, accounting software, or payment processor data. Some use platforms with independent data verification, which speeds up underwriting and often results in better terms for qualified businesses.

Asset-based lending is a financing method where businesses secure loans using their own assets—accounts receivable, inventory, equipment—as collateral rather than relying on cash flow or credit history alone. It's one of the most flexible ways for companies to access working capital, especially when traditional bank loans aren't an option.

This guide covers how ABL works, what assets qualify as collateral, the benefits and drawbacks to consider, and how to manage a facility once it's in place.

Asset-based lending (ABL) is a financing method where a business secures a loan or line of credit using its balance sheet assets—like accounts receivable, inventory, or equipment—as collateral. Unlike traditional bank loans that focus primarily on cash flow or credit history, ABL lets companies tap into the value of what they already own.

The loan amount depends on the appraised value of the pledged assets. Lenders typically advance higher percentages for liquid assets like receivables and lower percentages for harder-to-sell assets like machinery. So a company with strong assets but uneven cash flows can often access more capital through ABL than through conventional financing.

Three terms come up constantly in ABL conversations:

Think of the borrowing base as a ceiling that moves up or down depending on your collateral. As your receivables grow, so does your available credit. As they shrink, the ceiling drops.

The ABL process looks different from traditional lending because lenders care more about collateral quality than creditworthiness alone. Your financial statements still matter, but the central question is different: what assets do you have, and how quickly could a lender convert them to cash if things went sideways?

An advance rate is the percentage of your collateral's value that a lender will actually fund. Accounts receivable from creditworthy customers might get an 80-85% advance rate, while inventory could range from 50-70% depending on how easily it sells.

Equipment and real estate typically receive lower rates because they take longer to liquidate. The logic is straightforward—a lender can collect on a 60-day invoice much faster than they can sell a piece of manufacturing equipment.

Your borrowing base is the total amount you can draw at any point, calculated by applying advance rates to your eligible collateral. Here's where ABL gets interesting: as your business grows and generates more receivables or inventory, your available credit grows automatically.

If you land a big contract and your receivables jump from $1 million to $2 million, your borrowing capacity increases proportionally. The financing scales with your operations without requiring a new loan application. For fast-growing companies, this alignment between business performance and financing capacity can be a significant advantage.

ABL facilities require regular reporting—often weekly or monthly—to verify collateral levels. Lenders may also conduct periodic field exams to audit your assets directly.

This creates operational overhead, though it also means lenders can offer more flexible terms since they're continuously monitoring their security. Many companies underestimate the time and systems required to produce accurate collateral reports on a consistent schedule. What starts as a manageable task can become burdensome as transaction volumes grow.

Not all assets work equally well for ABL. Eligibility depends on how quickly and reliably an asset can be converted to cash.

Lenders also exclude certain assets from eligibility. Receivables older than 90 days, invoices concentrated with a single customer, or amounts owed by related parties often don't count toward your borrowing base. The gap between your total assets and your eligible collateral can be substantial—sometimes surprisingly so.

ABL offers several advantages that make it attractive for certain business profiles. The benefits tend to compound for companies with the right asset mix.

Companies with valuable assets but inconsistent cash flow often access significantly more capital through ABL than traditional loans would allow. The focus on collateral rather than earnings history opens doors that might otherwise stay closed.

Consider a business with $5 million in receivables but thin margins. That company might struggle to get a $2 million traditional loan based on cash flow alone. Through an ABL facility, however, the same business could potentially access $4 million or more.

As your receivables and inventory increase, your credit availability increases proportionally. You're not locked into a fixed loan amount that you'll outgrow in six months.

This scaling mechanism creates a virtuous cycle for growing companies. More sales generate more receivables, which unlock more credit, which funds more growth.

ABL agreements typically include fewer and less restrictive financial covenants than conventional bank loans. Since the lender's security comes from the collateral itself, they're often less concerned with traditional metrics like debt-to-EBITDA ratios.

Businesses with cyclical revenue patterns can draw more heavily during peak seasons when receivables are high, then pay down during slower periods. The facility flexes with your business cycle rather than fighting against it.

Understanding the distinction between ABL and cash flow lending helps clarify when each approach makes sense. The two methods serve different business profiles.

Cash flow lenders want to see consistent, predictable earnings. Asset-based lenders want to see valuable, liquid collateral. Many businesses find that ABL provides access to capital when cash flow lending isn't available—or offers better terms when both options exist.

The choice often comes down to your company's profile. A seasonal business with lumpy revenue but strong receivables might find ABL more accessible. A SaaS company with predictable recurring revenue might prefer cash flow lending.

ABL isn't the right fit for every situation. The limitations are worth understanding before pursuing this path.

The operational burden of ABL can be significant. You'll need systems and processes to generate regular collateral reports, and your team will need to accommodate periodic lender audits.

Companies managing loans in spreadsheets often find the reporting requirements particularly challenging as transaction volumes grow. What once took a few hours can balloon into days of work each month.

Lenders apply strict eligibility criteria. Aged receivables, customer concentrations, certain inventory types, and intercompany balances often get excluded from your borrowing base.

A company might have $10 million in total receivables but only $7 million in eligible receivables after exclusions. Understanding these limitations upfront helps set realistic expectations about available credit.

While interest rates on ABL facilities can be competitive, the total cost of borrowing often includes additional fees for field exams, appraisals, unused line fees, and ongoing monitoring. These costs add up and factor into any comparison with other financing options.

ABL works well for specific business profiles. The fit depends on your asset mix, growth trajectory, and operational capacity.

Several characteristics tend to indicate a good ABL fit:

Certain sectors naturally generate the asset profiles that ABL lenders prefer. Manufacturing and distribution companies typically carry substantial inventory and receivables. Wholesale and retail businesses often have similar profiles.

Staffing and professional services firms generate steady receivables from ongoing client relationships. Transportation and logistics companies combine equipment assets with regular invoicing cycles. In each case, the industry's natural operations create the collateral that supports ABL facilities.

Once you have an ABL facility in place, operational execution becomes critical. The reporting and compliance requirements demand reliable systems and processes.

Accurate, current collateral data is the foundation of your borrowing capacity. Manual tracking often creates errors and delays that affect available credit.

Platforms like Cascade Debt provide independently verified data and real-time monitoring that support compliance while reducing operational burden. The ability to monitor your borrowing base daily—rather than scrambling to compile reports at month-end—enables faster decision-making and smoother lender relationships.

Manual borrowing base calculations are time-consuming and error-prone, especially as transaction volumes grow. What once took days of spreadsheet work can be reduced to minutes with the right automation tools.

Before implementing automated systems, many companies find themselves processing 100,000+ rows in complex Excel models. The time savings from automation frees your team to focus on higher-value activities instead of data processing.

Lenders value real-time visibility into collateral performance. Technology platforms that provide automated data feeds can strengthen lender relationships and potentially improve your terms—all without adding headcount to your operations team.

The transparency piece matters more than many borrowers realize. When your lender can see what's happening in real time, conversations about credit availability become much smoother. You're not waiting for month-end reports to identify issues or opportunities.

ABL works best when viewed as a strategic tool rather than just a financing product. The structure rewards growth: more sales mean more receivables, which means more available credit to fund additional growth.

This creates a cycle that can accelerate expansion in ways that fixed-amount loans cannot. The key is having the operational infrastructure to manage the facility efficiently.

Companies that invest in accurate data, automated reporting, and transparent lender relationships extract the most value from their ABL facilities. The operational foundation determines whether ABL becomes a growth accelerator or an administrative burden.

Platforms like Cascade Debt help originators and investors manage ABL facilities with precision, transparency, and automation. Get Started to see how real-time data and analytics can support your asset-based lending operations.

A manufacturer with $2 million in outstanding invoices from creditworthy customers could borrow up to $1.6 million (at an 80% advance rate) against those receivables. As the company generates new invoices, its available credit increases proportionally, funding production of additional orders without requiring a new loan application.

Timelines vary based on collateral complexity and lender requirements. Most businesses can expect four to eight weeks for a thorough due diligence process that includes asset appraisals, system integrations for reporting, and legal documentation.

If your collateral value drops below the borrowing base threshold, the lender may require you to pay down the outstanding balance or provide additional collateral. This situation is called an "overadvance," and most ABL agreements include specific provisions for how it gets resolved.

Startups with limited operating history often find ABL challenging since lenders require established, verifiable asset pools. However, companies with strong receivables from creditworthy customers may still qualify, even without extensive track records.

In commercial lending, the terms are often used interchangeably. However, "asset-backed" more commonly refers to securities backed by pooled assets (like mortgages or auto loans) in capital markets contexts, while "asset-based" typically describes direct lending to businesses secured by their own assets.

.png)

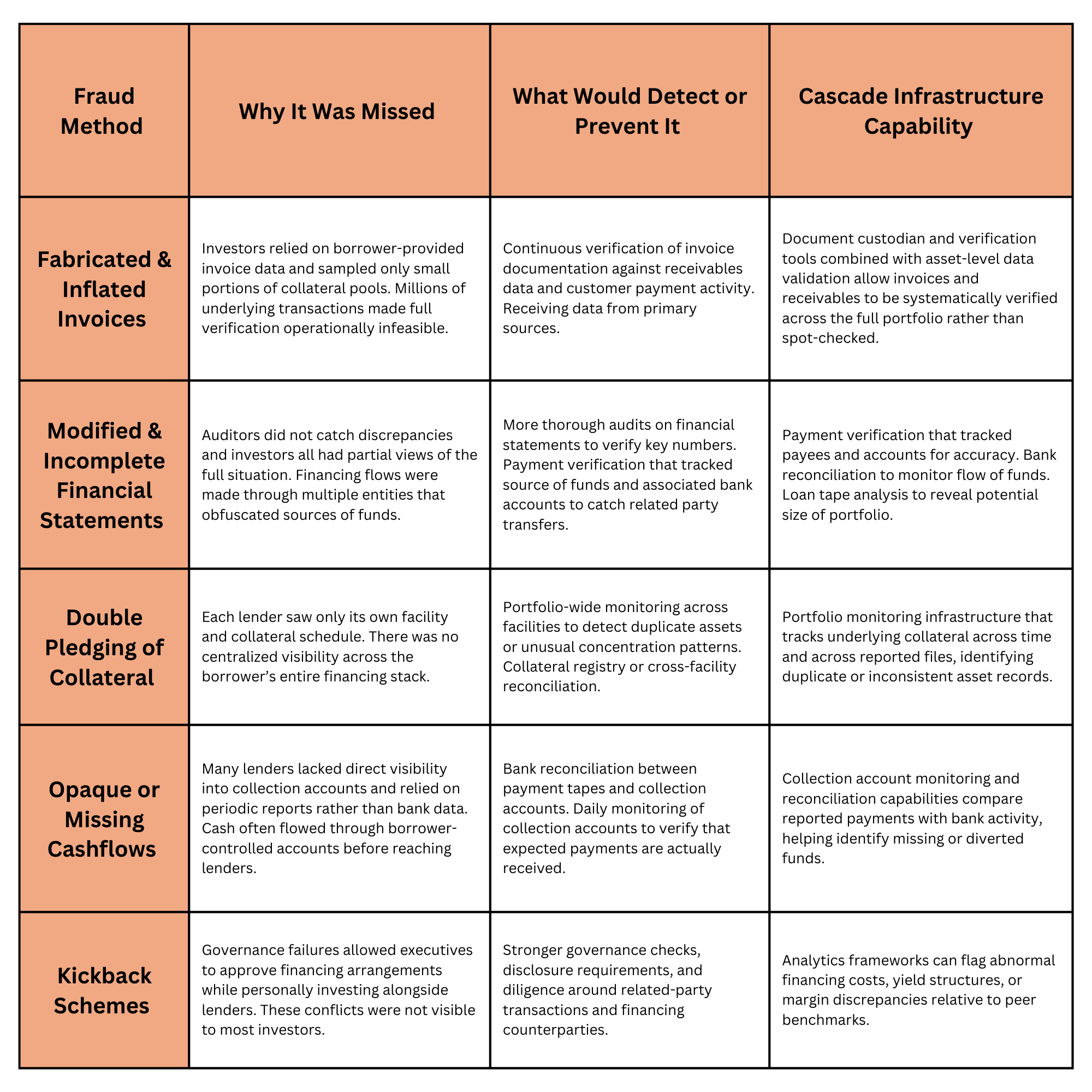

The collapse of First Brands Group represents one of the most significant alleged fraud events in private credit markets in recent years, with billions of dollars in exposure across banks, hedge funds, private credit funds, and supply chain finance providers.

Investigations and court filings point to several mechanisms used to misrepresent collateral and extract financing.

Prosecutors allege that First Brands fabricated invoices and inflated the value of legitimate invoices to obtain additional financing. In one documented example, a package of invoices worth $2.3 million was submitted with a value of $11.2 million, with some individual invoices inflated by 10x or more. Overall, roughly $2.7 billion in accounts receivable were fake or heavily manipulated at the time of bankruptcy.

First Brands executives would modify consolidated financial statements to reflect a “fraction” of the real accounts payables and receivables financing they had received.

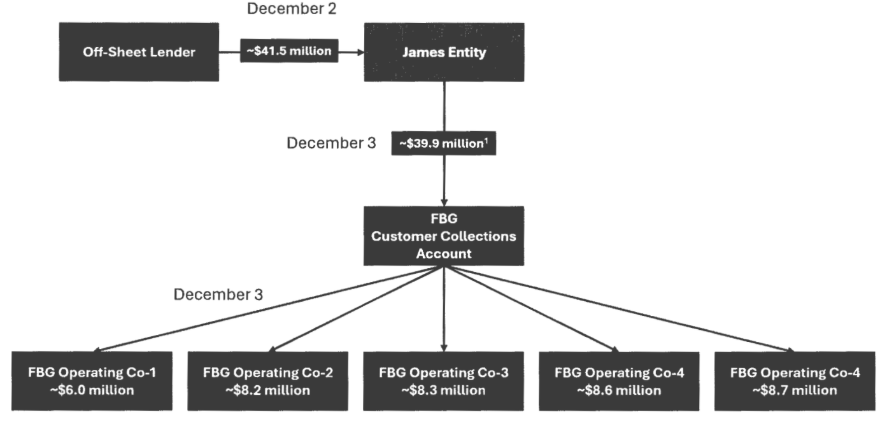

They also kept a lot of the financing completely off-balance sheet so that lenders would not know the scale of borrowing. This was accomplished with sale-leaseback arrangements using at least three connected entities. These entities would receive funds from the partner since they held the receivables but would funnel the cash and rights to the receivables back to First Brands. Amounts were sent to operating entities and made to look like they came from customers to avoid being seen as the related party transactions they were.

Below was an example of how funds flowed from a lender to the related entity to the master collections account and then to operating accounts:

Executives are accused of pledging the same receivables and loan collateral multiple times across different financing facilities. This practice allowed the company to raise funding from multiple lenders using the same underlying assets. Such schemes are difficult to detect when lenders have visibility only into their own facility and there is no centralized monitoring of the full collateral pool.

One of the most troubling aspects of the case involves missing or unaccounted-for cash flows. Court filings suggest that approximately $2.3 billion in receivable payments cannot be fully traced.

Even at the height of the bankruptcy, when lenders asked whether funds had been transferred to segregated collection accounts, First Brands’ counsel reportedly responded:

“We don’t know.”

“US$0.”

First Brands also used “round-tripping”, where they would pay off delinquent invoices using funds from elsewhere to make it appear that customers were paying.

One of the main financiers to First Brands, Onset Financial, is alleged to have had a kickback scheme arranged with a First Brands VP (who was also brother to the CEO). Onset would provide short-tern loans with upfront payments that had up to 300% IRRs, then divert some of those profits to the brother. Onset was reported to have lent out $2.5 billion and received $2.9 billion from these deals. According to a January 9 lawsuit, he expected to earn approximately $130 million in profit from these investments.

Some employees were aware that something was off. In a September 2022 message sent days after Edward James agreed to an inventory loan with an alleged 179% internal rate of return, a First Brands employee wrote “‘dude .. whoever sold that onset deal to us is [Onset] employee of the century,’”

In hindsight, several indicators suggested areas of potential suspicion:

Fraud in ABL transactions can usually be found in three main areas:

To mitigate fraud, Cascade is guided by three main principles:

Cascade’s Deal Infrastructure suite was created specifically to mitigate fraud on deals and includes:

For more information, check out the one-pager at the link here.

Managing private credit facilities with spreadsheets works until it doesn't. When you're processing 100,000+ rows of receivables data, tracking dozens of eligibility rules, and calculating borrowing base figures that shift daily, manual approaches create bottlenecks that limit growth and introduce costly errors.

Private debt software automates the complex calculations, covenant monitoring, and reporting that asset-based lending demands. This guide covers what these platforms do, the features that matter most, and how to evaluate whether a solution fits your business.

Private debt software helps lenders and investors manage, monitor, and report on private credit facilities. These platforms pull data from originator systems, track whether borrowers are meeting their loan agreements, assess portfolio risk, and generate reports for internal teams and external stakeholders. Unlike traditional loan management systems built for bank lending, private debt software focuses on asset-based lending—facilities secured by receivables, inventory, or other collateral that changes daily.

The distinction matters more than you might expect. A borrowing base (the amount a borrower can draw based on eligible collateral) shifts constantly as new receivables come in and old ones age out or get paid. Concentration limits cap how much exposure a facility can have to any single customer or industry. Eligibility criteria determine which receivables actually count toward the borrowing base. Generic loan software wasn't designed to handle this level of complexity.

Private debt platforms bring together several core capabilities:

Standard loan software falls short when a credit facility is secured by thousands of individual receivables, each with its own eligibility status, aging profile, and concentration impact. The complexity isn't just about volume. It's about the interconnected rules that govern what counts toward the borrowing base at any given moment—and how quickly those calculations change.

Borrowing base calculations sit at the heart of asset-based lending. These calculations determine how much a borrower can draw against their facility based on eligible collateral, minus reserves and concentration limits. Eligibility criteria can include dozens of rules: receivable age, obligor concentration, geographic limits, dilution rates, and more.

Many teams still manage these calculations in spreadsheets. Processing 100,000+ rows with complex formulas takes significant time and creates room for error. One misplaced formula can throw off the entire calculation. Specialized software automates this work, applying eligibility rules to current data and producing accurate borrowing base figures in minutes rather than days.

Both originators and investors benefit from current data on portfolio performance. Month-old reports don't provide much value when market conditions shift or portfolio metrics approach covenant thresholds. Real-time monitoring means stakeholders can see delinquency trends, concentration changes, and eligibility shifts as they happen.

This visibility serves different purposes depending on who's looking. Originators can identify issues before they become covenant breaches. Investors gain confidence that their capital is being deployed according to agreed-upon terms. The transparency reduces friction and builds trust between counterparties—which matters when it's time to expand the facility or bring in additional capital partners.

When originators and investors rely on the same metrics for decision-making, the source of that data matters. Independent, third-party verified data eliminates disputes over calculations and provides a neutral foundation for the relationship. Neither party has to wonder whether the numbers have been adjusted or interpreted favorably.

This neutrality becomes especially valuable during facility amendments, covenant discussions, or when bringing in new capital partners. Everyone works from the same verified dataset, which speeds up negotiations and reduces the back-and-forth that can slow down deals.

Buyers evaluating private debt software encounter a range of capabilities. Understanding what each feature does—and why it matters—helps separate essential functionality from nice-to-have additions.

Analytics tools assess concentration risk, delinquency trends, vintage performance, and portfolio stratification. Vintage performance tracks how loans originated in a specific time period perform over their lifecycle. Portfolio stratification breaks down the portfolio by characteristics like credit score, loan size, or geography.

These capabilities help credit teams identify emerging issues and make informed decisions about facility management. For example, if delinquencies are rising in a particular geographic region or customer segment, the analytics surface that trend before it affects overall portfolio performance.

Covenant compliance monitoring tracks financial covenants, portfolio triggers, and reporting deadlines automatically. Rather than manually checking each requirement against current data, the platform alerts stakeholders when metrics approach or breach thresholds.

Common covenants in asset-based facilities include minimum portfolio yield, maximum delinquency rates, concentration limits, and dilution caps. Automated tracking reduces the risk of surprise covenant violations and gives teams time to address issues proactively.

Generating investor-ready reports often consumes significant time each month or quarter. Teams that previously spent 40+ hours on monthly reporting can complete the same work in a fraction of the time with pre-built templates and automated data population.

Beyond time savings, consistent reporting formats make it easier for investors to compare performance across periods and facilities. The reduced manual work also means fewer errors and less time spent reconciling discrepancies.

Modern platforms connect directly to originator systems through native integrations with common database types—SQL, PostgreSQL, MongoDB, and cloud-based data warehouses among them. Direct connectivity eliminates manual file transfers, reduces errors, and enables more frequent data refreshes.

Platforms with integrations to 20+ database types offer flexibility for diverse originator technology stacks. This matters because originators often use different systems for loan origination, servicing, and accounting. The ability to pull data from multiple sources into a single platform simplifies operations considerably.

Software that assists with modeling facility terms, eligibility criteria, and waterfall structures during deal setup accelerates time to close. Waterfall structures determine the order in which cash flows are distributed to different parties—senior lenders get paid before subordinated lenders, for example.

Some platforms also help teams better understand loan documents and support negotiation and structuring processes. This guidance proves particularly valuable for originators newer to institutional capital relationships who may not have extensive experience with complex facility documentation.

For fund managers, mark-to-market capabilities and portfolio valuations support NAV (net asset value) calculations and investor reporting. Private credit valuation software provides the methodology and documentation needed for auditor review and regulatory compliance.

Valuation in private credit differs from public markets because there's no readily available market price. Platforms that provide consistent, defensible valuation methodologies help fund managers meet their reporting obligations while maintaining credibility with investors and auditors.

Comprehensive platforms cover every stage from initial due diligence through ongoing portfolio management. This end-to-end approach eliminates the need to stitch together multiple point solutions, each with its own data format and user interface.

Before facility close, software supports initial credit analysis, data tape review, and risk assessment. A data tape is a detailed file containing loan-level information about every receivable or loan in a portfolio. Teams can evaluate historical performance, stress test portfolios under different scenarios, and identify potential issues during the underwriting process.

At closing, platforms configure borrowing base rules, covenant thresholds, eligibility criteria, and reporting requirements. This setup phase establishes the foundation for ongoing monitoring. Getting the configuration right upfront saves significant time and prevents disputes later.

Daily or weekly monitoring tracks eligibility, concentrations, and portfolio performance against facility terms. Automated alerts notify stakeholders when metrics change materially or approach covenant limits. This ongoing visibility allows both originators and investors to stay informed without constant manual checking.

Payment tracking, fee calculations, and reconciliation with servicer data round out the administrative capabilities. Reconciliation ensures that the data in the platform matches what the servicer reports—catching discrepancies early before they compound into larger issues.

Different users have different priorities when evaluating private debt software. Understanding these perspectives helps both sides of a transaction find common ground on platform selection.

Automation reduces manual loan operations work, enabling growth without proportional team expansion. Before adopting specialized software, many originators manage their loans in Excel. Processing complex models with 100,000+ rows takes significant time and creates bottlenecks as the portfolio grows.

With purpose-built platforms, originators often see meaningful efficiency gains:

This efficiency allows teams to manage larger portfolios and additional capital relationships without expanding headcount proportionally. The ability to monitor borrowing base daily and expedite the fundraising process with lenders enables faster expansion.

Investors receive independent data feeds without adding operational burden to originators. This transparency builds confidence and reduces the back-and-forth requests that can strain relationships.

When investors can access current portfolio data directly, they spend less time chasing information and more time on strategic decisions. The originator benefits too—their team isn't fielding constant data requests or preparing ad-hoc reports. Both parties get what they want without creating extra work for either side.

Selecting the right platform requires evaluating several factors beyond feature lists. The best fit depends on your specific situation, technology stack, and growth plans.

Consider whether the platform provides independently verified data that both originators and investors can rely on. This neutrality matters when multiple stakeholders make decisions based on the same metrics. A platform that serves as a neutral data agent between parties can reduce friction and speed up negotiations.

Assess database connectivity and typical onboarding timelines. Platforms with native integrations to common database types can complete setup in days or weeks rather than months. Ask about the specific systems you use and the vendor's experience connecting to them. Implementation speed varies significantly based on data complexity and the number of source systems involved.

Evaluate whether the platform can handle increasing receivable volumes, additional facilities, and new capital partners. Growth shouldn't require re-platforming or significant additional investment. Ask how current clients have scaled on the platform and what that process looked like.

The right private debt software reduces operational complexity while supporting business expansion. Teams move from managing spreadsheets to managing strategy. Capital partners gain the transparency they want without creating additional work for originator teams.

For originators and investors seeking a platform built specifically for asset-based finance, Cascade Debt offers a comprehensive solution trusted by over 100 clients worldwide, monitoring more than $25 billion in receivable balances.

Implementation timelines vary based on data complexity and integration requirements. Modern platforms with native database connectors can complete setup in days or weeks rather than months, depending on the number of source systems and the complexity of facility terms.

Leading platforms offer native integrations with common database systems including SQL, PostgreSQL, MongoDB, and cloud-based data warehouses. Direct connectivity eliminates manual file transfers and enables more frequent data refreshes.

Private debt software is purpose-built for asset-based facilities with features like borrowing base calculations, concentration tracking, and covenant monitoring. General loan management systems typically lack the dynamic eligibility rules and real-time calculations that asset-based lending requires.

Yes, some platforms provide independently verified data that both parties can rely on for decision-making. This neutrality eliminates disputes over metrics and calculations, which speeds up negotiations and builds trust between counterparties.

Platforms handling sensitive financial data and personally identifiable borrower information typically maintain enterprise-grade security certifications and encryption standards. Ask vendors about their specific certifications and security practices during the evaluation process.

Platforms apply eligibility criteria and concentration limits to current receivables data, automatically calculating available borrowing capacity as the underlying portfolio changes. This automation replaces manual spreadsheet calculations that can take hours or days to complete.

Tape cracking is a core diligence function focused on transforming raw originator data into a reliable, decision-ready dataset. It occurs before pricing, structuring, or capital commitment, and its purpose is not optimization or enhancement. The objective is simple but critical: establish confidence in the data itself.

At its core, tape cracking answers a single diligence question: Can we trust this tape to reflect real portfolio behavior, based not only on the data itself, but on the quality, structure, and consistency of how that data is presented?

Before any modeling assumptions or yield projections are applied, investors need assurance that the underlying loan-level data is complete, internally consistent, and representative of how the portfolio has performed.

The first step in tape cracking is standardizing loan tapes into a consistent schema. This includes normalizing dates, balances, statuses, identifiers, and relationships across files that are often delivered in inconsistent or ad hoc formats.

Common tape issues are addressed at this stage, including missing or duplicated loans, inconsistent status logic, and invalid balances or timelines that violate basic loan mechanics. Loan, customer, and transaction data are aligned so that entities reconcile correctly, ensuring that loan-level records can support downstream analysis without distortion.

The goal is not to reshape the data to fit expectations, but to ensure it is structurally sound and analytically usable.

Once data is normalized, a configurable suite of validation tests is applied to assess data integrity. These tests are categorized by severity and risk impact.

Validation checks span missing data, formatting errors, and logical inconsistencies. Tests can be customized by client, asset class, or deal structure, allowing diligence teams to align validation rigor with risk tolerance and investment strategy.

Every pipeline run produces a data health snapshot that is stored historically. Validation results can be downloaded by date or exported in aggregate for internal engineering, risk, or diligence teams.

Reports clearly document what data was excluded, what data was processed with warnings, and where assumptions or gaps exist. This creates audit-style visibility into data quality and eliminates ambiguity around how the dataset was constructed.

For investors, validation reporting provides a defensible record of diligence decisions and data tradeoffs made before capital deployment.

Tape cracking extends beyond static loan attributes into transaction-level behavior. Collections data is mapped directly to individual loans and validated for timing, consistency, and completeness.

This process identifies mismatches between expected amortization and actual borrower cash behavior. Trends in gross collections, net collections, and volatility over time are monitored to surface structural or operational issues that may not be visible at the loan header level.

Reliable cash flow mapping is essential for understanding performance dynamics and for building accurate forward-looking assumptions.

Delinquency buckets are standardized across the portfolio to ensure consistent treatment of roll rates, cures, and charge-offs. This normalization prevents artificial performance distortion caused by inconsistent status definitions or reporting practices.

Observed cash flows are used to build CPR and CDR curves, allowing investors to identify front-loaded risk, seasoning effects, and shifts in borrower behavior over time. These insights are grounded in actual performance rather than modeled expectations.

Loans are grouped by origination vintage and age to enable cohort-based analysis. Comparing vintages helps isolate changes in underwriting quality, macro-driven performance shifts, and operational changes at the originator.

Divergence between early and recent vintages often provides early warning signals that aggregate portfolio metrics can obscure. Cohort analysis supports investment committee diligence by grounding risk discussions in empirical evidence rather than anecdotal explanations.

Flexible filters allow portfolios to be sliced by geography, loan size, term, risk tier, and product type. Investors can stress specific subsets, identify concentrations, and run “what-if” diligence scenarios quickly.

These filters remain reusable post-close, supporting ongoing monitoring and enabling consistency between pre-close diligence and post-close surveillance.

Validation-driven tape cracking surfaces data risk before capital is deployed, reducing diligence friction and eliminating avoidable back-and-forth with originators. It prevents post-close surprises by ensuring that investment decisions are based on verified data, not assumptions.

Most importantly, it establishes a clean foundation for investment committee decisions, ongoing portfolio monitoring, and the ability to scale exposure over time with confidence.

Cascade acts as an independent data and validation layer during diligence, bridging the gap between raw originator data and investor-grade analysis. The focus is not on improving optics, but on transparency, early risk identification, and repeatable, defensible diligence workflows.

By systematizing tape cracking and validation, Cascade enables investors to move faster without compromising data integrity, and to build long-term confidence in both their datasets and their decisions.

Document verification serves as the first line of defense in any master servicing workflow for structured finance facilities. Before a single loan can be included in a borrowing base calculation, we must confirm that the underlying documentation is authentic, consistent, and meets all facility eligibility criteria.

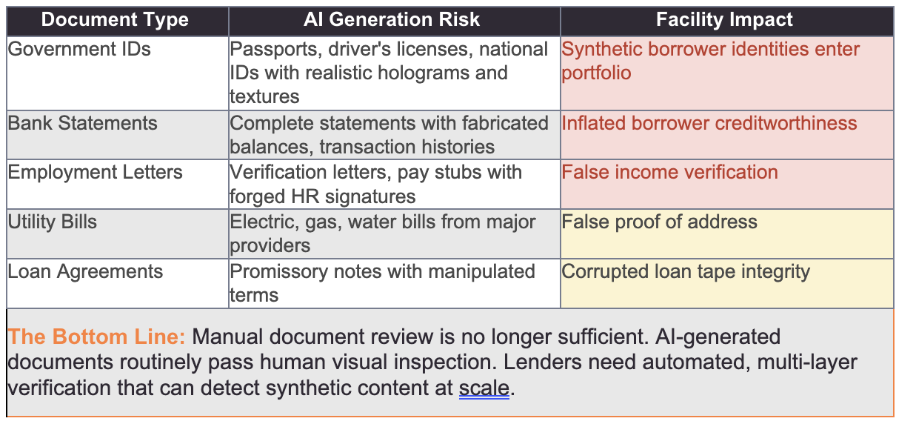

In 2025, this mission has become dramatically more complex. The emergence of sophisticated AI image generation tools—including Google's Gemini (Nano Banana), ChatGPT's DALL-E, Midjourney, and others—has fundamentally changed the threat landscape. Fraudsters can now generate convincing fake identity documents, bank statements, employment letters, and loan agreements in minutes, with no technical expertise required.

At Cascade, we actively monitor emerging fraud vectors, including AI-generated synthetic documents. We're continuously evaluating detection technologies and refining our verification processes to stay ahead of these evolving risks.

The document verification challenge has evolved beyond simple forgery detection. Today's threat comes from generative AI tools that can produce near-perfect synthetic documents at scale.

Research from Sumsub's Q1 2025 Identity Fraud Report reveals alarming statistics:

Every document type in a loan verification package can now be synthetically generated:

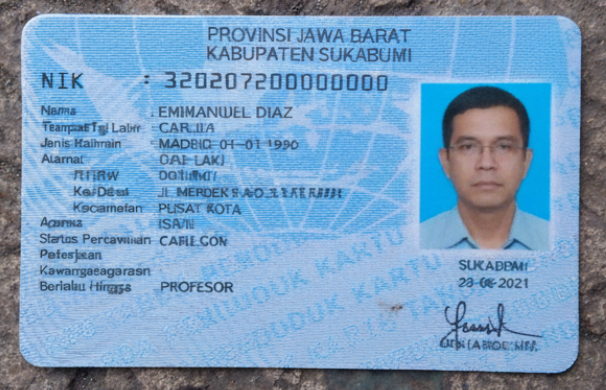

Gemini’s content filtering is highly inconsistent, changing its responses based on language, timing, or slight wording shifts. Because the system reacts to keywords instead of context, even standard business research can be incorrectly flagged or blocked. To demonstrate the severity of the AI fraud threat, and Cascade's detection capabilities, we conducted a controlled test using Google's Gemini image generation tool (Nano Banana).

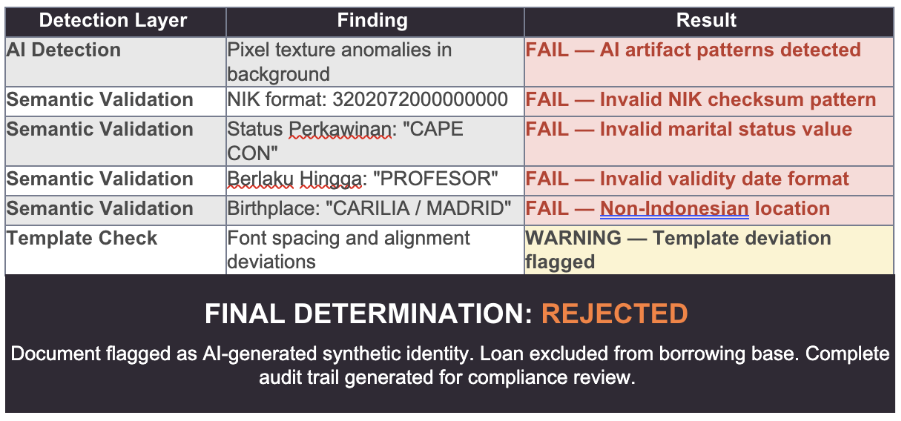

Using simple text prompts, we generated a fake Indonesian national identity card (Kartu Tanda Penduduk or KTP) in under three minutes. The prompt requested a realistic-looking ID photographed on a surface—the type of image commonly submitted for KYC verification.

At first glance, this document appears authentic. It includes:

This is exactly the type of document that would pass manual visual inspection in a traditional KYC process.

Our four-layer verification system identified multiple fraud indicators:

The emergence of AI-generated document fraud has fundamentally changed the risk landscape for structured finance facilities. Synthetic identity documents can now be created in minutes by anyone with access to consumer AI tools. Traditional manual verification methods are no longer sufficient.

Cascade's document verification solution addresses this new reality with a four-layer approach that combines:

This eliminates the historical trade-off between verification thoroughness and operational speed. Lenders gain confidence in collateral authenticity. Originators gain scalability without fraud exposure. Both gain the transparency and audit trails that modern structured finance demands.

Contact Cascade to schedule a demonstration of our AI-powered document verification solution.

All statistics cited in this white paper have been verified from the following authoritative sources:

[1] Sumsub Q1 2025 Identity Fraud Trends

"Synthetic Identity Document Fraud Surges 300% in the U.S. - Sumsub Warns E-Commerce, Healthtech and Fintech at Risk"

https://sumsub.com/newsroom/synthetic-identity-document-fraud-surges-300-in-the-u-s-sumsub-warns-e-commerce-healthtech-and-fintech-at-risk/

[2] Sumsub Identity Fraud Report 2025-2026

"Fraud Trends for 2025: From AI-Driven Scams to Identity Theft and Fraud Democratization"

https://sumsub.com/blog/fraud-trends-sumsub-fraud-report/

[3] Deloitte Center for Financial Services

"Generative AI is expected to magnify the risk of deepfakes and other fraud in banking"

https://www.deloitte.com/us/en/insights/industry/financial-services/deepfake-banking-fraud-risk-on-the-rise.html

[4] AllAboutAI - AI Fraud Detection Statistics 2025

"AI Fraud Detection Statistics 2025: 50x Faster Detection & 98% Accuracy"

https://www.allaboutai.com/resources/ai-statistics/ai-fraud-detection/

[5] Google DeepMind - SynthID

"SynthID - Tools for watermarking and identifying AI-generated content"

https://deepmind.google/models/synthid/

[6] Google Blog - AI Image Verification

"How we're bringing AI image verification to the Gemini app"

https://blog.google/technology/ai/ai-image-verification-gemini-app/

[7] Google Blog - SynthID Detector

"SynthID Detector: Identify content made with Google's AI tools"

https://blog.google/technology/ai/google-synthid-ai-content-detector/

All demonstration data is fictional. The AI-generated document shown was created solely for illustrative purposes.

As private credit portfolios scale, so does the operational burden of ensuring every loan, payment, and collateral movement aligns with investor and lender expectations. Cascade’s Deal Infrastructure Suite was built to centralize those workflows, offering full visibility, automated controls, and verifiable data across the servicing lifecycle.

From daily cash tracking to collateral verification, the suite replaces spreadsheets and manual checks with real-time, data-driven oversight.

Cascade’s Loan Verification module automatically validates loan-level data against supporting documents such as agreements, schedules, and payment files to confirm eligibility and detect discrepancies before they impact funding or compliance. This creates a transparent audit trail for all stakeholders and reduces reliance on manual sampling.

The Payment Reconciliation tool matches incoming borrower payments and outgoing investor distributions against loan schedules and bank statements in real time. By automatically reconciling transactions, the module highlights missing, duplicate, or misallocated payments, ensuring accurate cash flow tracking and simplifying investor reporting.

Cascade’s Cash Management module provides a secure, rules-based environment to manage account hierarchies, sweep structures, and cash movements. It ensures that collections, reserves, and disbursements flow according to facility covenants and predefined permissions, minimizing operational risk while improving transparency for lenders and servicers.

With Collateral Registration, originators and lenders can register pledged assets with government registries to establish legal rights over the collateral securing each facility. This includes filing trust assignments and receivable lists with systems like Mexico's RUG (Registro Único de Garantías Mobiliarias) or Indonesia's fiducia registry (AJIB). The module tracks filing deadlines, ensures timely submissions, and maintains proof of completed registrations. It circulates confirmation documents to all relevant parties and verifies and monitors pledged assets across facilities.

Cascade’s Backup Loan Servicing module acts as a safeguard for investors and lenders by maintaining a live, verified copy of portfolio data. In the event of a servicer disruption, Cascade can step in seamlessly, ensuring continuity of borrower management, collections, and reporting. The module also enables investors to monitor loan performance independently without relying solely on the primary servicer’s data.

Together, these modules form a unified framework for Master Servicing, bridging the gap between primary servicers, trustees, and investors. With standardized data, automated controls, and transparent audit trails, Cascade enables financial institutions to scale confidently while maintaining the integrity of every loan, payment, and collateral record.

Private credit has scaled to $1.5 trillion in 2024, and with that growth comes more opportunities for fraud to slip through. Higher deal volumes, more complex portfolio structures, and faster transaction timelines all create gaps. That is why Cascade built a systematic fraud prevention framework designed to verify every data point, every asset, and every transaction, not just a random sample.

Our fraud checklist spans the full asset lifecycle, from origination and data onboarding to cash management and investor reporting.

Whether you are an originator, investor, or trustee, Cascade provides the confidence that every dollar and every document aligns. The platform reduces operational risk, strengthens investor trust, and protects portfolios from fraud before it happens.

Asia’s private debt market continues to scale rapidly, fuelled by a growing base of non-bank lenders, development finance institutions (DFIs), and a new generation of private credit funds focused on fintech, MSME, and sustainable finance opportunities across the region.

To help bring clarity to this dynamic and fragmented space, we’ve published the 2025 Asia Debt Investor Market Map, featuring banks, DFIs, microfinance-backed platforms, and private credit funds actively deploying capital across the region.

This is the latest release in our global series, following the USA and LATAM editions and is part of our effort to map out who’s funding what, and where, across emerging and established credit markets.

We’ve organized the market into four primary categories:

This Asia edition follows our US and LATAM market maps, each designed to bring transparency to this growing corner of capital markets. We’ll be releasing the Africa Debt Investor Market Map in the coming weeks to complete this four-part series.

Think your firm should be included? Or looking to get introduced to any of the investors listed? Reach out - we’d be happy to connect.

In today’s fast-moving financial environment, teams rely on various tools and processes for data management, risk assessment, and reporting. Unfortunately, these workflows can sometimes be slowed down by data inconsistencies, delays, or manual procedures that introduce errors.

Cascade is designed to seamlessly fit into your existing workflows, acting as a flexible backbone that ensures your data is accurate, timely, and reliable, ultimately streamlining your operations and supporting better decision-making.

Many organizations utilize Business Intelligence (BI) tools like Power BI, Looker, or Tableau to visualize and analyze their loan and financial data. However, raw data exports often need to be cleaned and validated to ensure accuracy which can be a time-consuming and error-prone process.

Cascade integrates directly into your workflow by providing customized, validated data exports. This ensures the data you import into your BI environment is both current and precise, reducing manual corrections and accelerating your analysis cycles.

Internal reports for risk and investment committees are crucial for strategic decisions. Typically, these reports are tailored to organizational needs and require regular updates.

Cascade supports this by offering customizable report templates that organizations can quickly download, adapt, and update. Built with embedded formulas and real-time data links, these reports deliver accurate, organization-specific insights, allowing your teams to access current data for more effective decision-making.

Managing complex structures like SPVs involves detailed accounting entries and reconciliations. Manual processing can lead to errors, delays, and compliance issues.

Cascade helps automate this process by enabling automated extraction of relevant data, which can be exported into accounting-ready formats for systems like QuickBooks. This ensures that your journal entries are accurate, timely, and consistent, supporting smoother financial operations.

These examples highlight just some of the ways Cascade integrates with and improves existing workflows. Whether you're handling investor reporting, loan servicing, portfolio analytics, compliance, or data reconciliation, Cascade offers adaptable solutions that can be tailored to your organization's unique needs.

By embedding into your workflows, Cascade provides:

In short, Cascade helps your organization leverage trusted, accurate data so you can focus on making informed decisions, managing risk, and growing your business.

In the highly complex and data-driven world of asset-backed loans (ABL), even the smallest errors can lead to massive overstatements of collateral—sometimes exceeding a million dollars. These "phantom" borrowing bases can distort risk assessments and lead to unintended exposures, all stemming from tiny data discrepancies.

Most service providers, whether treasury management firms or loan administrators, do not perform the core calculations themselves. Instead, they depend on third-party data providers and automated systems to supply the critical figures: the outstanding principal balance of receivables and the days past due (DPD). Given the sheer volume of daily data—transactions, reversals, updates—manual validation is practically impossible. That’s why specialized data companies are essential, using sophisticated validation processes to maintain accuracy.

Why Small Errors Are So Dangerous

With thousands or millions of data points flowing daily, tiny inaccuracies can slip through unnoticed. Over time, these discrepancies can compound, creating seriously inflated collateral values that aren’t rooted in reality. And in large, long-term facilities, these small errors can go undetected for months or even years.

Consider a facility that operated for over a year, generating more than 15 gigabytes of raw data files. Every day, the originator sent two files to the lender:

The automated system that produced these files had a subtle flaw:

However, instead of reversing the split, the system mistakenly inserted the full $100 into principal during the reversal. This incorrect entry increased the outstanding balance by $100, and because the reversal didn't properly split the payment, an extra $10 of principal remained unadjusted.

Over thousands of transactions, these small errors accumulated. After over a year and countless files, the false collateral value—based on these inflated balances—surpassed $1 million. Neither the lender nor the originator recognized the discrepancy until a thorough reconciliation uncovered the error.

This example underscores the critical need for dedicated data validation and reconciliation services. Relying on manual checks or simple pivot tables isn’t enough to catch systemic errors in large, complex data sets. Automated validation tools like Cascade can identify these discrepancies immediately, making errors obvious before they grow into significant financial risks.

The bottom line: Tiny data errors can create massive, hidden risks. Employing advanced validation systems is essential to ensure data integrity and prevent phantom collateral from slipping through unnoticed.

Don’t let tiny data errors inflate your borrowing base. See how Cascade’s automated validation tools catch discrepancies before they cost you millions.

In asset-based lending, investors rely heavily on the numbers originators report. But why?

This breakdown explores the practical infrastructure, policies, and data strategies that support investor confidence and how Cascade enhances transparency and validation.

1. Excel is Still the Default

Most investors monitor portfolio performance through Excel-based reports. This means originators can deliver key metrics, like DPD and outstanding balance, without needing to expose every underlying input or calculation.

2. File Size and Complexity

Trying to recalculate DPD or outstanding balance at a granular level can make Excel files too large to use. Simplified summaries are not just preferred, they're required.

3. Trust in Loan Management Systems

Many originators use third-party or industry-standard Loan Management Systems (LMS) to run calculations. These systems are typically reviewed during deal diligence, giving investors confidence in the data’s consistency and structure.

4. Investors Can’t Always Rebuild the Math

Reconstructing loan performance data in-house requires infrastructure most capital providers don’t have. Instead, they rely on originators and tools like Cascade to validate figures based on raw inputs.

Calculation logic isn't always standardized.

This variability makes it essential for investors to understand originator policy, product structure, and data logic.

Cascade works behind the scenes to validate loan performance based on raw source data. By rebuilding repayment schedules using the original loan terms (even in cases of restructured or cash-modified loans) Cascade provides a level of validation investors rarely have time or tooling to perform themselves.

When investors must make decisions based on minimal datasets, Cascade brings clarity through structure and automation.

Two metrics matter above all: Days Past Due (DPD) and Outstanding Balance. These are not only the most important, they’re also the most auditable.

1. DPD: A Real-Time Signal of Portfolio Health

DPD tells investors how late payments are and how risky the portfolio might be.

DPD is also the foundation for many early-warning systems. Learn more in our blog: How Default Rates Are Calculated

2. Outstanding Balance: The Exposure Anchor

Outstanding balance reflects the amount of capital still at risk.

It’s used for:

Key considerations:

When clients pay ahead of schedule, balances should fall in line with or outperform expectations.

Investors don’t blindly trust originators—they trust efficient infrastructure, validated systems, and policy alignment. Cascade strengthens that trust by validating data directly from the source and offering deeper insights into what’s at stake.

Looking to streamline how you validate and manage originator data?

Revenue-based funding lets businesses access capital by pledging a percentage of future revenue rather than giving up equity or putting up collateral. Payments flex with your actual sales—higher when business is strong, lower during slower months.

This guide covers how revenue-based funding works, who it's best suited for, and the tradeoffs you'll want to weigh before pursuing it.

Revenue-based funding is a type of financing where investors provide capital in exchange for a percentage of a company's ongoing gross revenues. Unlike traditional loans with fixed monthly payments, repayments rise and fall based on how much revenue your business actually generates. This makes it particularly well-suited for subscription-based businesses or e-commerce companies with predictable cash flow.

The arrangement continues until you've repaid a predetermined cap—typically 1.1x to 1.5x the original funding amount. So if you receive $500,000 with a 1.3x cap, you'll repay $650,000 total, regardless of how long it takes.

What sets revenue-based funding apart from other financing options is that founders keep full ownership of their company. There's no equity stake given up, no board seats surrendered, and no dilution of your ownership percentage. Here's what defines this model:

The mechanics are straightforward once you understand the core components. Let's walk through how a typical arrangement unfolds.

A funding provider advances you a lump sum based on your monthly recurring revenue or gross revenue. The amount you qualify for typically ranges from one to six months of your average monthly revenue, though this varies by provider and your business profile.

The repayment cap represents the total amount you'll pay back—your original funding plus a fee. This cap is fixed at the outset, so you know exactly what you owe from day one.

Each month, a fixed percentage of your revenue—typically 1-10%—is automatically collected. During a strong month, you pay more and accelerate your payoff. During a slower month, your payment decreases, giving your cash flow room to breathe.

Once you've paid back the full cap amount, the funding relationship ends. There's no ongoing obligation, no lingering interest accrual, and no balloon payment waiting at the end.

For the right business, revenue-based funding offers advantages that traditional financing can't match.

You maintain complete ownership of your company. For founders who've worked hard to build something valuable, this means not giving away a piece of the upside when your business eventually exits or scales significantly.

This is where revenue-based funding truly shines. If your revenue dips during a slow season or unexpected downturn, your payments automatically decrease. You're not stuck making a fixed payment that strains your cash flow when you can least afford it.

While bank loans can take weeks or months to close, many revenue-based funding providers make decisions within days. The underwriting process relies heavily on your revenue data, which can be verified quickly through integrations with your accounting software or payment processors.

Traditional bank loans often require personal guarantees or asset collateral. Revenue-based funding typically doesn't—your future revenue serves as the basis for the arrangement, keeping your personal assets separate from your business financing.

Revenue-based funding is designed for companies investing in growth initiatives like marketing spend, inventory purchases, or hiring. It's capital meant to generate returns, not fund long-term infrastructure projects.

No financing option is perfect for every situation. Understanding the limitations helps you make an informed decision.

Because you're paying back a multiple of what you borrowed, the effective cost often exceeds what you'd pay on a traditional bank loan. A 1.3x cap on a 12-month repayment translates to a significantly higher annualized rate than most term loans.

Revenue-based funding providers evaluate your ability to repay based on existing revenue patterns. If you're pre-revenue or have inconsistent sales, you likely won't qualify. This isn't startup funding—it's growth capital for businesses with traction.

Since your funding amount ties directly to your current revenue, you might not access as much capital as you'd get through equity financing or a large credit facility. For major expansion plans, revenue-based funding might only cover part of what you're looking for.

Many providers collect daily or weekly rather than monthly. While this smooths out cash flow in some ways, it also requires consistent revenue and careful cash management to avoid shortfalls.

Revenue-based funding works exceptionally well for certain business models while being a poor fit for others.

Predictable monthly recurring revenue makes repayment modeling straightforward for both you and the provider. The subscription model's inherent predictability is exactly what revenue-based funding is designed around.

Steady transaction volume provides the reliable revenue stream that supports percentage-based repayment. Seasonal businesses can still qualify, though providers will factor in revenue fluctuations.

Higher gross margins mean you can absorb the percentage-based repayment without squeezing your operating budget. A business running on thin margins might find the revenue share too constraining.

If maintaining ownership is a priority—whether for personal reasons or because you believe your equity will be worth significantly more later—revenue-based funding lets you access growth capital without giving up a stake.

Before applying, it helps to understand what providers typically look for during underwriting.

Most providers set a floor for monthly revenue, though the specific amount varies widely. Higher revenue generally means access to larger funding amounts and potentially better terms.

Providers want to see operating history to assess your revenue stability and trajectory. A longer track record with consistent growth strengthens your application.

You'll provide access to financial records, bank statements, or accounting software. Providers that use independently verified data can often move faster and offer more competitive terms because they have higher confidence in the numbers.

Funding amounts typically range from one to six months of your monthly revenue, though some providers go higher for established businesses with strong metrics. The specific amount depends on your revenue consistency, business model, and the provider's risk assessment.

Stronger documentation and verified data can improve your funding terms. When providers can independently confirm your revenue figures, they're often willing to offer larger amounts or lower repayment caps.

The application process is generally faster than traditional lending, but preparation still matters.

Gather your revenue documentation, bank statements, and accounting records before you start. Platforms that provide independently verified data can streamline this process significantly.

Complete the provider's application with your business information and revenue details. Many providers offer online applications that take 15-30 minutes.

Review repayment caps, revenue share percentages, and terms across multiple providers. The lowest cap isn't always the best deal—consider the revenue share percentage and how it affects your monthly cash flow.

Once you agree to terms, funds typically arrive within days. Some providers can fund within 24-48 hours of approval.

If revenue-based funding doesn't fit your situation, several other financing options might work better.

Modern platforms have transformed how revenue-based funding transactions happen. Real-time data integration and automated reporting allow providers to verify revenue, monitor performance, and manage risk far more efficiently than manual processes ever could.

For originators and investors in the revenue-based funding space, technology solutions that provide independently verified data and real-time monitoring support faster, more transparent funding decisions. Platforms like Cascade Debt enable this kind of infrastructure, helping both sides of the transaction operate with greater confidence and efficiency.

Revenue-based funding offers flexible, non-dilutive capital for businesses with proven revenue streams. The key is honestly assessing whether your revenue history and business model align with what providers look for.

If you're an originator or investor looking to streamline revenue-based funding operations with verified data and real-time analytics, Get Started with Cascade Debt.

Your payments decrease proportionally since they're tied to a percentage of revenue. This built-in flexibility protects businesses during slower periods—you won't face a fixed payment you can't afford when revenue is down.

Revenue-based funding is structured as debt because it requires repayment. However, it doesn't involve giving up ownership like equity financing, which is why it's often called "non-dilutive" capital.

Generally, no. Revenue-based funding requires demonstrated revenue history for underwriting. Pre-revenue startups typically explore other options like equity financing, grants, or convertible notes.

Providers typically require access to bank statements, accounting software, or payment processor data. Some use platforms with independent data verification, which speeds up underwriting and often results in better terms for qualified businesses.

Asset-based lending is a financing method where businesses secure loans using their own assets—accounts receivable, inventory, equipment—as collateral rather than relying on cash flow or credit history alone. It's one of the most flexible ways for companies to access working capital, especially when traditional bank loans aren't an option.

This guide covers how ABL works, what assets qualify as collateral, the benefits and drawbacks to consider, and how to manage a facility once it's in place.

Asset-based lending (ABL) is a financing method where a business secures a loan or line of credit using its balance sheet assets—like accounts receivable, inventory, or equipment—as collateral. Unlike traditional bank loans that focus primarily on cash flow or credit history, ABL lets companies tap into the value of what they already own.

The loan amount depends on the appraised value of the pledged assets. Lenders typically advance higher percentages for liquid assets like receivables and lower percentages for harder-to-sell assets like machinery. So a company with strong assets but uneven cash flows can often access more capital through ABL than through conventional financing.

Three terms come up constantly in ABL conversations:

Think of the borrowing base as a ceiling that moves up or down depending on your collateral. As your receivables grow, so does your available credit. As they shrink, the ceiling drops.

The ABL process looks different from traditional lending because lenders care more about collateral quality than creditworthiness alone. Your financial statements still matter, but the central question is different: what assets do you have, and how quickly could a lender convert them to cash if things went sideways?

An advance rate is the percentage of your collateral's value that a lender will actually fund. Accounts receivable from creditworthy customers might get an 80-85% advance rate, while inventory could range from 50-70% depending on how easily it sells.

Equipment and real estate typically receive lower rates because they take longer to liquidate. The logic is straightforward—a lender can collect on a 60-day invoice much faster than they can sell a piece of manufacturing equipment.

Your borrowing base is the total amount you can draw at any point, calculated by applying advance rates to your eligible collateral. Here's where ABL gets interesting: as your business grows and generates more receivables or inventory, your available credit grows automatically.

If you land a big contract and your receivables jump from $1 million to $2 million, your borrowing capacity increases proportionally. The financing scales with your operations without requiring a new loan application. For fast-growing companies, this alignment between business performance and financing capacity can be a significant advantage.

ABL facilities require regular reporting—often weekly or monthly—to verify collateral levels. Lenders may also conduct periodic field exams to audit your assets directly.

This creates operational overhead, though it also means lenders can offer more flexible terms since they're continuously monitoring their security. Many companies underestimate the time and systems required to produce accurate collateral reports on a consistent schedule. What starts as a manageable task can become burdensome as transaction volumes grow.

Not all assets work equally well for ABL. Eligibility depends on how quickly and reliably an asset can be converted to cash.

Lenders also exclude certain assets from eligibility. Receivables older than 90 days, invoices concentrated with a single customer, or amounts owed by related parties often don't count toward your borrowing base. The gap between your total assets and your eligible collateral can be substantial—sometimes surprisingly so.

ABL offers several advantages that make it attractive for certain business profiles. The benefits tend to compound for companies with the right asset mix.

Companies with valuable assets but inconsistent cash flow often access significantly more capital through ABL than traditional loans would allow. The focus on collateral rather than earnings history opens doors that might otherwise stay closed.

Consider a business with $5 million in receivables but thin margins. That company might struggle to get a $2 million traditional loan based on cash flow alone. Through an ABL facility, however, the same business could potentially access $4 million or more.

As your receivables and inventory increase, your credit availability increases proportionally. You're not locked into a fixed loan amount that you'll outgrow in six months.

This scaling mechanism creates a virtuous cycle for growing companies. More sales generate more receivables, which unlock more credit, which funds more growth.

ABL agreements typically include fewer and less restrictive financial covenants than conventional bank loans. Since the lender's security comes from the collateral itself, they're often less concerned with traditional metrics like debt-to-EBITDA ratios.

Businesses with cyclical revenue patterns can draw more heavily during peak seasons when receivables are high, then pay down during slower periods. The facility flexes with your business cycle rather than fighting against it.

Understanding the distinction between ABL and cash flow lending helps clarify when each approach makes sense. The two methods serve different business profiles.

Cash flow lenders want to see consistent, predictable earnings. Asset-based lenders want to see valuable, liquid collateral. Many businesses find that ABL provides access to capital when cash flow lending isn't available—or offers better terms when both options exist.

The choice often comes down to your company's profile. A seasonal business with lumpy revenue but strong receivables might find ABL more accessible. A SaaS company with predictable recurring revenue might prefer cash flow lending.

ABL isn't the right fit for every situation. The limitations are worth understanding before pursuing this path.

The operational burden of ABL can be significant. You'll need systems and processes to generate regular collateral reports, and your team will need to accommodate periodic lender audits.

Companies managing loans in spreadsheets often find the reporting requirements particularly challenging as transaction volumes grow. What once took a few hours can balloon into days of work each month.